In March 2025, a Missouri senior citizen was about to close on a property. He got an email from his title company with wire instructions for over $1.3 million. The title company name was right. The branding was right. The instructions were not. The email was a spoof, and the account was a fraudster’s. The FBI’s Recovery Asset Team got the call in time and froze the account before the money disappeared. That story sits in the FBI’s 2025 IC3 Annual Report, released April 6, 2026, in the section the Bureau uses to highlight wins. It’s a win because someone moved fast. Most files don’t get that ending.

The IC3 report came out last month, and the numbers underneath that one story are not subtle.

What the report lays out

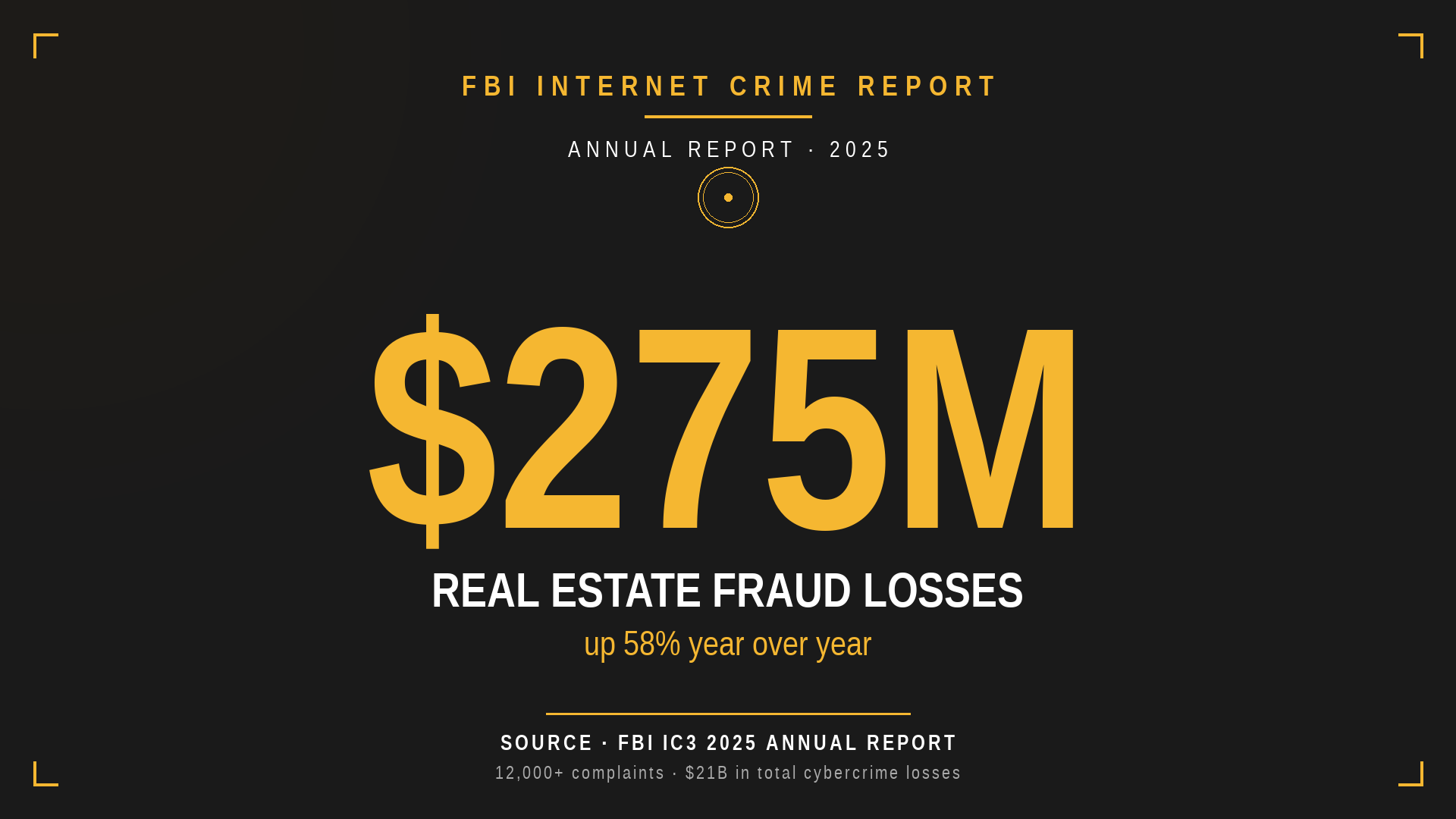

In 2025, IC3 took more than 1 million complaints and recorded $20.9 billion in losses across all cybercrime categories. That’s a 26% jump in losses over 2024 in a single year. Real estate fraud was its own line item, with 12,000+ complaints and $275 million in losses. The 2024 number for real estate was $174 million across 9,000+ complaints.

Losses up 58%. Complaints up 32%. The closing table just had its worst year on record, and the FBI is putting that in writing.

If you read those two numbers next to each other, you can feel where this is heading. More cases, bigger cases, faster. The average reported loss per real estate complaint also climbed, from roughly $19,000 in 2024 to roughly $22,000 in 2025. There are simply more deals being targeted, and when a target hits, it hits for more.

Where the money actually moves

The IC3 report breaks out, for each major fraud type, how the money left the victim’s account. For Business Email Compromise, which is the umbrella the closing table sits under, 86% of losses moved by wire transfer or ACH. Cryptocurrency accounted for 7%. Debit and credit cards, 3%. The remaining few percent split across peer to peer transfer, prepaid cards, checks, and cash.

Read that again. Eighty six percent of BEC losses move through the same rails the closing table uses. Wires and ACH are not the side door for these schemes. They are the front door. Whatever else fraudsters are doing across the rest of the IC3 dataset, when they go after a closing, they go after the wire.

BEC overall had nearly 25,000 complaints and $3 billion in losses in 2025, second only to investment fraud. Real estate is one slice of that pie, and it’s the slice every attorney and agent reading this lives in. The IC3 report itself uses the label “BEC/Real Estate” when categorizing several of its 2025 case studies, including the Missouri closing above and a separate August 2025 case where a buyer wired more than $449,000 to a fraudster impersonating their attorney.

AI is no longer the future tense

The IC3 2025 report has its own section on AI now, which is the first time that’s been true at this scale. More than 22,000 complaints in 2025 included a confirmed AI element. Adjusted losses topped $893 million.

Inside that, BEC scams with an AI component cleared $30 million in losses in 2025 alone. Voice cloning is called out by the FBI directly, used to mimic a CEO, an attorney, or a family member to push a wire. The Bureau also flags AI generated emails that look indistinguishable from a real one, with perfect grammar, branding lifted from real email threads, and tone calibrated to match a specific person.

AI does not invent a new attack at the closing table. It scales the old one. The same wire fraud playbook from five years ago, only now the email is cleaner, the spoofed call sounds like the partner you’ve worked with for a decade, and the attacker is running it against ten files at once instead of one. As I covered in Issue #2 on video deepfakes in real estate, the detection cues people used to rely on, broken English, off voice, awkward phrasing, are not the safety net they used to be.

Recovery is not a plan

The FBI report makes the case for prevention louder than any vendor ever could. The Recovery Asset Team initiated 3,900 Financial Fraud Kill Chain incidents in 2025, covering $1.16 billion in attempted theft. They froze $679 million. That’s a 58% success rate, and that’s the best number the FBI has.

That success rate only holds when the victim, the bank, and IC3.gov all move within hours, not days. The Kill Chain is a sprint, not a process. Most files don’t move that fast. By the time the buyer realizes the wire went to the wrong account, the money has often hopped through one or more domestic banks and is on its way overseas, frequently to Hong Kong or another jurisdiction outside the FBI’s reach. The Bureau’s own case study on the Missouri closing notes that the fraudulent recipient had already been instructed to send $1 million to a fraudulent account in Hong Kong before the freeze landed.

The takeaway is plain. Recovery is the backstop, not the plan. Every plan for protecting a closing has to assume that the wire, once gone, is gone.

What actually stops it

Tricks expire. Systems don’t.

At Chicago Title, prevention starts with delivering wire instructions through inHere instead of email, and a hard rule to our clients: no wire instruction is ever new, ever changed, or ever confirmed by email alone. Do not wire on what you see in any email until you’ve called us to verify, and use a number from our website or your closing disclosure, never a number an email gave you. That callback discipline, on the client’s side, is the safety net the entire wire fraud playbook is built around defeating. The wire instruction discipline is the part that’s been load bearing for years and is what the IC3 numbers should reinforce for everyone in this chain. The Missouri case in the IC3 report worked because someone made the call. It would have worked even better if the call had happened before the wire instead of after.

For attorneys and agents, the move is to point your client directly at the title company before the wire goes out. The title company is who issued the instructions, so the title company is who confirms them. Not back to a number in the email. Your client calls the title company on a number they got from the title company’s own website or the closing disclosure, and they confirm the destination out loud before the wire goes.

The pattern that protects every transaction is the same one. Deliver wire instructions through a channel the email thread cannot reach into. Confirm receipt by phone, on a number nobody in the email can spoof. None of that is new. The IC3 report is the data point that makes it non negotiable.

The bigger picture

The IC3 dataset is not a forecast. It’s a tally of what already happened. $275 million walked off the closing table in 2025, up 58% in a year, and the AI category went from a footnote in past reports to its own chapter in this one. That trajectory does not reverse on its own.

The pattern across this series has been the same. Wire fraud in Issue #1, deepfake video in Issue #2, fake power of attorney and vacant land impersonation in Issue #3. Different mechanics, same vulnerability: a real person who is never actually in the room. The IC3 2025 report is the FBI’s confirmation that the gap is widening, not closing.

If you’re seeing this pattern on your desk, let’s talk. The pattern recognition is the value, and there’s more of it on every transaction.

Frequently asked questions

How much did real estate fraud cost in 2025 according to the FBI?

The FBI’s IC3 2025 Annual Report recorded $275 million in real estate fraud losses across more than 12,000 complaints, up from $174 million and 9,000+ complaints in 2024. That’s a 58% increase in losses and a 32% increase in complaints in one year.

How do criminals move stolen funds in business email compromise schemes?

According to the IC3 2025 report, 86% of BEC losses moved by wire transfer or ACH, 7% by cryptocurrency, and 3% by debit or credit card. Wire transfers and ACH are the same rails real estate closings use, which makes the closing table the highest value target in the BEC category.

How much was lost to AI-related fraud in 2025?

The FBI received more than 22,000 complaints in 2025 with a confirmed AI element, totaling $893 million in losses. Within that, BEC scams with an AI nexus accounted for more than $30 million in losses.

What is the FBI’s Financial Fraud Kill Chain and how successful is it?

The IC3 Recovery Asset Team’s Financial Fraud Kill Chain freezes funds at recipient banks when victims, banks, and law enforcement coordinate quickly. In 2025, the team initiated about 3,900 incidents covering $1.16 billion in attempted theft and froze $679 million, a 58% recovery rate. Speed is the entire game. The process only works when the wire is reported within hours.

What is the most common form of real estate wire fraud?

Business email compromise targeting the buyer’s wire instructions is the dominant pattern. A criminal monitors or spoofs an email thread, sends fraudulent wire instructions branded to look like the title company or attorney, and the buyer wires funds to the fraudster’s account. Once the wire clears, recovery is unlikely.

How can buyers and sellers protect themselves at closing?

Treat every wire instruction received by email as suspect until verified by phone using a number you obtained outside email, ideally a number provided in person or on the title company’s website. Never trust a number embedded in an email. Use platforms that deliver wire instructions through verified channels rather than email attachments. Confirm the receipt of funds with the title company before assuming the wire landed.

Why are AI scams hard to detect at closings?

AI generated emails have correct grammar, match the writing style of real participants in the email thread, and reproduce branding accurately. Voice cloning can mimic a known attorney or title officer on a phone call. The detection cues people relied on in past years, such as broken English or off voices, are no longer reliable. Verification through known channels is the only consistent defense.